Using the example of where a legatee has been given £5000 subject to IHT calculated at £100

Go to the relevant legatee and add the pecuniary legacy and enter the net figure of £4900. In the narrative field say something like “Legacy of £5000 less IHT of £100 as per clause 4 of the Will”

If ALL residuary beneficiaries are paying IHT...

If all the residuary beneficiaries are due to pay IHT then the full amount of IHT paid, which would include the £100, will be included as an Administration Expense.

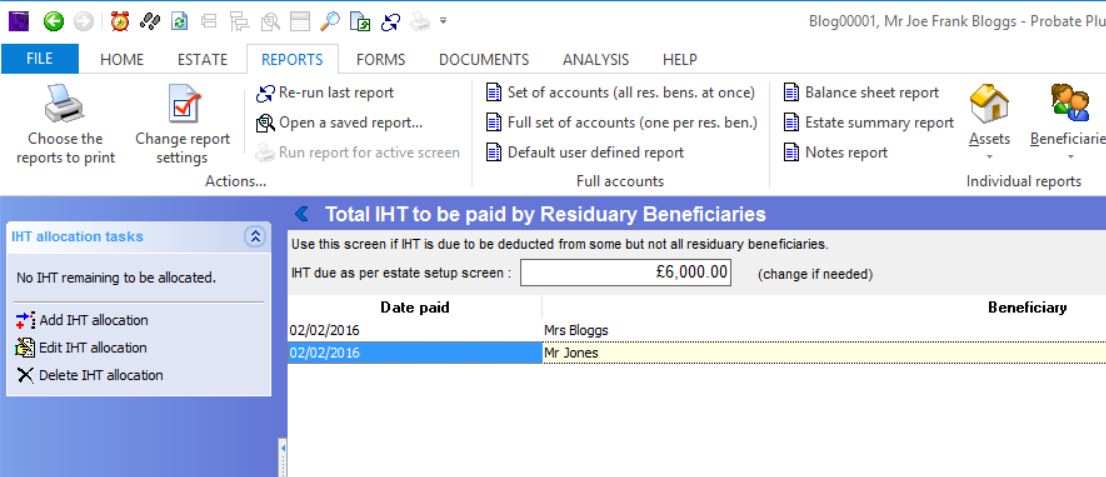

If only SOME beneficiaries are paying IHT

If a residuary beneficiary is exempt (ie a widow or a charity) then it would be necessary to use the IHT Payment function. Here one would first enter the full amount of the IHT paid.

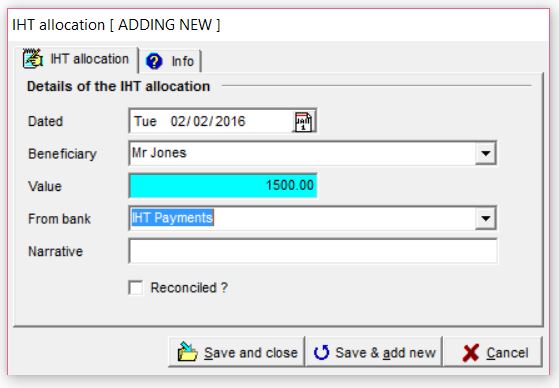

The next step is to work out each residuary beneficiary’s liability and allocate each share accordingly debiting a cash account which could be called IHT payments as in the illustration below.

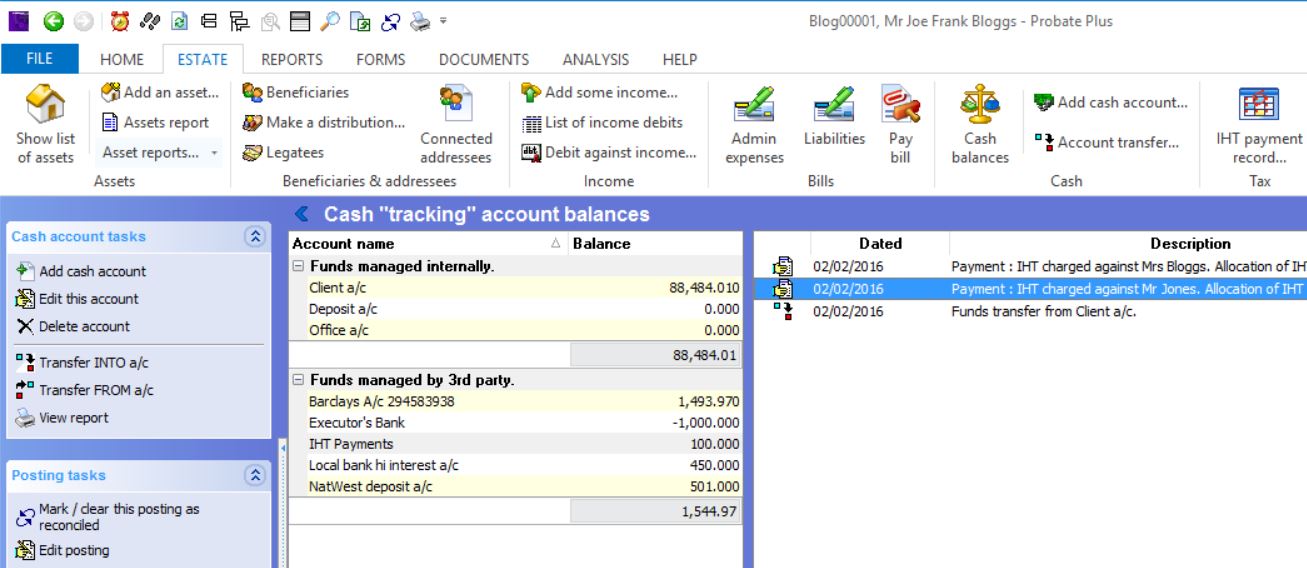

To round up the cash accounts, using the transfer between accounts function, you would transfer from client account or whichever account was debited when paying the IHT and credit the IHT account.

In the example it would end up showing an outstanding balance of £100 which is of course the amount due from the legatee.

You would then just enter an expense to show the £100 paid to HMRC from the IHT payments cash account which will bring that account's balance back to zero.